The ever-increasing cost of compulsory motor third-party liability insurance compels owners who sell cars to return the unused portion of insurance. An avalanche of questions falls upon specialized forums and official websites of insurers. The latter comment on this topic without much desire and even more reluctantly give recommendations. CTP return for car sales is, of course, possible, but there are a number of features, the observance of which will facilitate the procedure.

Norms and Rules

To return CTP when selling a car, you must be guided by the following documents:

- Federal Law of 04.25.02 as amended on 05.06.2016 “On Compulsory Third Party Liability Insurance of Vehicle Owners” (Article 10);

- OSAGO rules developed by the Central Bank of the Russian Federation and the Regulation of the Bank of Russia (No. 431).

And a few more immutable truths:

- The new owner has only ten days to renew the vehicle.

- The seller of the vehicle is obliged to inform the insurer about the completed contract of sale.

- The Regulation on compulsory motor liability insurance (clause 1.9) notifies clients of insurance companies that a change of vehicle or policyholder is not provided for in compulsory motor liability insurance. That is, under the circumstances described, the insurance contract terminates the legal effect. And this is the basis for the refund of OSAGO when selling a car.

- Insurance indemnities, whether they were or not, are not taken into account in case of termination of the contract.

- Documents confirming the change of vehicle owner are required to be submitted to the policyholder.

- The contract concluded for the transportation of the vehicle to the place of registration cannot be terminated.

- The contract can be terminated only if it was concluded for a year.

Where to begin

MTPL refund when selling a car, if there is a serious reason, is prescribed in the MTPL rules, paragraph 33.

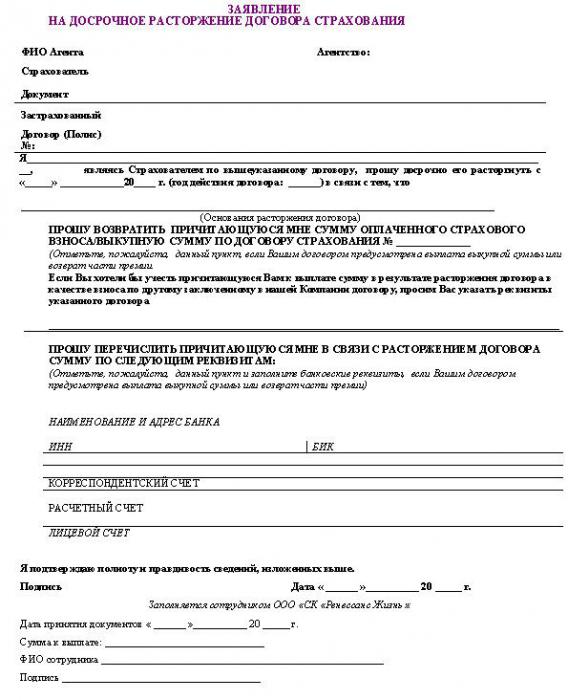

The return of the unspent amount of insurance for the UK is very disadvantageous. Therefore, experts recommend seeking help from lawyers. The procedure requires a specific set of documents. One of them is a statement. He is written by a person who has concluded an agreement with an insurance company. The application form has no established form. Therefore, each insurance company offers its own developed form. But, in general, the application for OSAGO refund when selling a car contains the following information: passport data of the insured, data on the insured vehicle, number of the insurance contract. A special point is the indication of the grounds for termination of insurance. Next, you will need the details for the transfer of funds (name of the bank, BIC, personal, correspondent and settlement accounts, etc.).

The body of the application consists of a request for termination of the insurance contract due to the sale of the vehicle, and, as a result, a change of ownership. Further, the applicant must indicate two amounts: which he did not manage to use, and which he made in the form of insurance premiums. The statement ends with a request to make a refund on the above details.

Each application must be registered as an incoming document. Car lawyers recommend that you make yourself a copy of the application, with the prescribed incoming number and date of admission. You can submit an application in person, or by registered mail through the Russian post. In this case, it is necessary to request a notification of delivery and draw up a detailed inventory of the attached documents. The second option is especially convenient if documents are not accepted at the office.

If the application is not accepted

Cases of refusal to accept an application and a package of documents for insurance return have been registered. Managers send customers to the head office: they, like, are not authorized to do this. It is not true. For the termination of the contract is one of the simple procedures, which is executed in any office of the insurance company. Be it regional, subsidiary or any other.

Documents for OSAGO return when selling a car

They are conditionally divided into two parts. One of them - the main one, is required in any insurance company, regardless of the reason for termination of the contract. The second, indicates and confirms that OSAGO is required when selling a car.

The base part includes the following documents:

- the original and notarized copy of the passport of the client who has drawn up the contract;

- an insurance policy that will be closed (only the original, it’s advisable to leave a copy for yourself that may be needed for the trial);

- receipt or electronic document confirming payment of CTP;

- Details of the bank and account to which the refund will be made (cash operations are prohibited).

The list of documents confirming the sale of the vehicle can be found in the insurance company itself. But usually it is:

- reference account (if the sale process is ongoing);

- Title with a change of ownership and a registered contract of sale.

The date of return of the MTPL insurance premium when selling a car will be considered the day of filing the package of documents.

Speaking of TCP. The manager of the SC has no right to demand its original or copy. Legislatively, the fact of the sale of the vehicle is confirmed by the contract of sale.

The timing

MTPL insurance return for car sales takes several business days. Each company brings this information to the client at the end of the receipt of documents.

But an IC client should know that almost any procedure performed by an insurance company cannot exceed 14 days. This norm is indicated in paragraph 34 of the CTP Rules. Otherwise, penalties are imposed on the UK, and the refund amount will increase due to the penalty imposed. If the insurance company delays its decision, then the client can file a written complaint with the Central Bank of the Russian Federation (in person or through the website), with the Union of Auto Insurers or with a lawsuit (in the place of registration of the SK office). The court very slowly considers such cases, so auto lawyers recommend starting with the Central Bank.

In rare cases, insurance companies may refuse to refund the amount of compulsory motor liability insurance when selling a car. This can be affected by a number of certain circumstances.

Vehicle owners in a hurry to sell them faster should understand that if the owner has already changed by the time the return is paid, then he will receive the money. Car lawyers strongly recommend that you first resolve all issues with the insurance company, and then arrange the vehicle for a new owner.

But for this the law has only ten days. There is every reason not to be in time, so experienced car owners are advised to take a receipt from the new owner on the return of compensation for compulsory motor liability insurance and enter it into the policy.

Refunds are issued not only to the insured

To receive the remaining amount of the cost of the policy, except for the policyholder can:

- the successor of the insured, recognized by a notary;

- legal representative from the insured;

- legal representative from the owner;

- heir to the owner of the vehicle, recognized by a notary.

Representatives must, when applying for OSAGO return, present a general power of attorney. Moreover, it must necessarily contain a clause stipulating the possibility of conducting monetary operations.

Formula for calculating the amount of return

On the Internet there are many sites offering a quick calculation of the cost of unused OSAGO. But you can do it manually. There is an official formula.

It looks like this:

D = (P - 23%) x (H ː 12), where:

- 23% - standard indicator of insurance company (implies certain expenses of the insurer);

- N - the number of full months until the end of the insurance contract;

- P is the total cost of the policy;

- D - amount of return.

Interest rates are determined by decree of the Central Bank of the Russian Federation. They are distributed as follows.

The costs of the insurer include a 3% deduction in PCA. For what? This amount is transferred to the reserve accounts from which compensation is paid. Moreover, 2% is the current reserve, and one is guaranteed.

20% remain in the company. They go for running expenses and customer affairs. This includes servicing the policyholder, accompanying the insurance policy, its manufacture, use of various equipment, salaries of employees who draw up documents, etc.

That is, the basis for the calculation is the remaining 77%.

The countdown date is the date the insured appeals to the company’s office. The day of signing the contract of sale is considered ideal.

Auto lawyers advise you to conduct independent calculations in advance in order to file a lawsuit in case of fraud by the insurance company.

Small digression

Legally, these same 23% are not defined anywhere. For example, the return of compulsory motor third-party liability insurance when selling the Rosgosstrakh car confirms that there is a “mutual agreement” between the parties. In any case, the situation is nervous. Now about 20% going to the insurer. If the insurance contract is not terminated early, where does the insurance company get these percentages? After all, the expenses seem to be the same? That is, the grounds for levying these percentages for early termination are completely unclear. The question hangs in the air. If, according to our own calculations, the amount should be paid large, then it makes sense, guided by Article 958 of the Civil Code of the Russian Federation and Clause 34 of the CTP Rules, to file a lawsuit with the court and demand that the funds paid for the policy be returned without taking into account these 20%.

Oddly enough, most of these claims are resolved positively by the court, since (see above) the law does not give clear indications of insurance companies retaining 23%.

In this case, you will need to pay a state fee. But when filling out an application for the return of the CTP insurance policy when selling a car, the collection of the state duty amount is also executed.

Ingosstrakh offers its own scheme

Clients who insure civil liability in Ingosstrakh Insurance Company, first of all, inform about their intentions by phone. The company manager clarifies the situation and gives advice, including on the package of documents necessary for termination. As soon as they are ready, the policyholder arrives at the nearest office, fills in the application form, which describes the reasons for termination and indicates the details for the return of a part of the cost of the policy.

If failure, then why?

As a rule, this is a late appeal for calculating the return of OSAGO when selling a car. If more than 60 days have passed since the sale of the vehicle, the insurance company has the right to refuse. Here it is necessary to take into account that the insurer will not calculate from the date of sale of the vehicle, but from the day of contacting the company that issued the policy.

Also, the insurance company will refuse to pay in case of sale of a car by general power of attorney. For legally the owner of the vehicle remains the same.

Interesting nuances

Some insurance companies offer to transfer the remaining CTP to a new policy. This question is right to decide the client himself.

Do I need a bonus?

But in any case, lawyers draw the attention of motorists to such a feature as KBM. This is the bonus malus coefficient accrued for a safe ride. This happens only at the end of the insurance year. And, as you know, the higher the CBM, the greater the discount awaits the policyholder when buying a new policy.

However, in case of early termination of the MTPL agreement, no matter for what reason, the bonus-malus coefficient is not accrued. Therefore, it is worth considering. Perhaps if two to three months are left before the policy expires, it is better to leave the contract valid and give yourself (if there are no offenses on the road) a discount in the form of an increased KBM.

Is it possible to save?

You may not have to issue a CTP insurance refund when selling a car (while retaining 23% of the deductible insurance tax). If there is confidence in the buyer, then CTP will simply be reissued, and the new owner will return the unused insurance. For this, a written agreement is concluded between the old and the new owner on the return of a certain amount. She is certified by a notary. You can go the other way and fix the inclusion of the new owner in the current OSAGO policy as a separate clause in the contract of sale. The buyer in this case writes a statement in which he asks to include it in a specific policy.

And, by the way, the insurer does not have the right to impose additional deductions if payments were made according to the policy for the occurrence of insured events.

And finally

The Russian Union of Auto Insurers warns car owners who sell them. Enough cases of fraud are already known: the new owners of the vehicle manage to return unused insurance (paid by the previous insurer) to themselves. Therefore, you can’t pull with paperwork in the UK!