In accordance with domestic law, all organizations are required to keep free finances in the bank. In this case, most of the settlements of legal entities should be made among themselves in non-cash form. For cash turnover, you need a cashier, an employee who will work with her, and a book in which transactions will be recorded. Next, we consider in more detail the features of filling out the documentation.

Cash book: why is it needed and how to keep it?

As practice shows, in most organizations cash flow is carried out in non-cash form. However, this does not mean at all that cash is not used in the course of these companies. If there is at least a small percentage of transactions concluded using banknotes, then the company must have a cash book. How to keep this journal? Who should enter information into it? These questions worry many entrepreneurs. It should be noted that according to the law since 2014, enterprises that have an income and expense accounting journal may not issue orders for cash operations. Accordingly, a cash book, a sample of the filling of which will be described later, may not be kept by them. Nevertheless, some entrepreneurs continue to use it. However, many organizations carry out its compilation incorrectly. In order to avoid problems with the tax inspection, sanctions and other penalties, you should be very careful about the operations performed and know how to keep the cash book correctly.

Normative base

Prior to the entry into force of the new recommendations on the accounting of cash transactions in the legislation, there were no direct indications that all entrepreneurs should have a cash book. A sample fill was also not installed. In the practice of arbitration courts, there have been cases when the decision was made in favor of entrepreneurs who did not take into account cash transactions in the journal. Since 2012, the Procedure for filling out a cash book has been adopted. The instruction prescribes the mandatory existence of a transaction journal for all entrepreneurs, regardless of which tax system they use if they make cash transactions. For incorrect compilation of documentation and other violations of accounting discipline that will be identified during the audit, a penalty may be imposed on the organization.

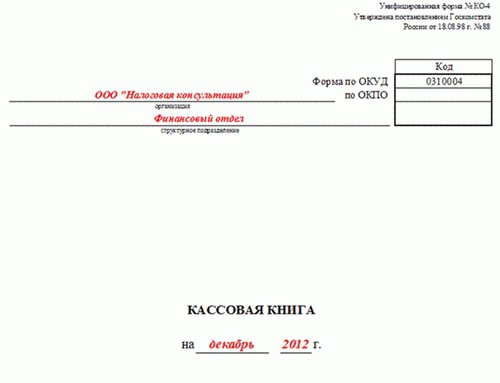

Document Feature

Before you tell how to keep the cash book correctly, you should explain what it is. From the above information, it is clear that this is a special journal for recording all cash transactions. In addition, the cash book is included in the list of documentation of financial statements. The resolution of the State Statistics Committee approved the form of the journal. It is called KO-4. The correct procedure for filling out the cash book is determined by the relevant Regulation. The regulations were approved by the Central Bank in 2011. Knowing how to keep a cash book correctly is very important, as supervisory inspections check it often enough. A new document is compiled for each year.

Sample filling out and maintaining the cash book: basic provisions

The document consists of 50 or 100 pages. As for the question of when you need to keep a cash book, it is established in accordance with the law that the journal is compiled from the beginning of the year and in increasing order. On the cover page the period of validity of the document is affixed. If the magazine ended before the end of the year, a new one is compiled. Records are not interrupted and continue with chronological sequence. The title page of the new journal indicates the start and end dates of its compilation. In this case, the sequence of documents will be easy to determine. As a rule, an enterprise acquires a ready-made cash book printed in a printing house with drawn columns and graphs. It is possible to compile a document in electronic form (how to keep a cash book in this format correctly will be described below). All pages are numbered immediately in the entire magazine. The total number of sheets is affixed at the end (on the last page). The indicated quantity is certified by the signatures of the boss and the person in charge. The stitched book is sealed with a wax or mastic seal.

Responsible person

The company has an employee who manages the cash book. How to properly maintain this journal is indicated in the relevant recommendations that the employee should know. This employee carries out cash transactions and enters information about them into the document. The completed sheet is verified by signature. This means that the employee assumes all responsibility for the operations performed and the information entered upon himself. At the end of the working day, the employee transfers the balance of cash to the accounting department. Together with it, all documentation is transferred - primary receipts and expenditures. The completed book sheet is also signed by the host accountant. If the latter is not at the enterprise, the signature is put by the head. This procedure is performed daily. In order to carry out cash transactions, a responsible officer authorized by the chief must be familiar with his duties, rights and responsibilities against signature. If we talk about how to keep a cash book of IP, then the process itself is similar to that carried out in the organization. However, the individual entrepreneur does not always provide for the staff, and in particular, there is not necessarily a person responsible for performing and recording cash transactions. If the IP works alone, then it carries out the reception and expenditure of funds. Accordingly, he makes entries in the journal himself and signs the completed pages. For those who do not know how to properly keep a cash book, the advice to the accountant presented below will help you navigate the requirements.

Title page

This page should contain the following information:

- For a legal entity - the full name of the organization, for a private entrepreneur - the full name of the entrepreneur, the name of the unit (if it is a branch).

- The duration of the journal. It can be a year or a certain date, if there are several documents.

- OKPO.

The inside of the document

Speaking about how to properly register a cash book, it should be noted that entries, both expendable and incoming, are made on one page. At the end of the day, the balance is reduced and the result is summed up. A report is compiled on the operations performed. Each sheet of the book consists of two parts with a tear line. The first half is the journal page in which information about operations is entered. In the second part, the cashier’s report is compiled . You can bend the sheet along the tear line and keep a carbon copy record. After entering the information, the sheet is cut. The first part of the page should be hemmed. Documents confirming operations are attached to the report (these papers are called the “primary”). For example, it can be an extract from the order, a cash receipt order, an application for an advance payment, a power of attorney, and so on.

Entering information in columns

At the top of the page should be indicated the date of entry of information. Filling out the sheet begins with a column, which indicates the balance at the beginning of the shift. Here is the amount that is transferred from the end of the previous page. Next, the serial number for the cash order is entered. It is indicated in the column "Document Number". The next line is the one to whom this paper was issued or from whom it was received. If this is an individual, then F.I.O. is introduced, if a legal entity is the name of the organization. The next column indicates the number of the offsetting account or subaccount. Enter information that indicates the method of receipt or expenditure of cash. For example, r / s - cf. 51, salary - cf. 70, customers and buyers - cf. 62. It should be noted here that these lines are not filled in by individual entrepreneurs.

Next are the columns "Consumption" and "Coming." They put down the amount in rubles in numbers. Pennies are indicated after the decimal point. For example, the amount of funds issued is as follows: 129.05 p. Each operation is recorded immediately after completion. Records are made only on the basis of primary documents. The column "Transfer" contains information on the amount of operations on the previous lines. In the end, you need to calculate the overall result. It is entered in the column "Total for the day." The result is calculated separately for the issued money and received funds. Next, the remainder is recorded. It is necessary to add up all the cash that arrived and remained from the previous day. From this amount, the issued funds are taken away. The figure written down in the book must coincide with the actual state of cash at the checkout. Those lines that remain free should be crossed out. This is necessary so that no one fills in the empty columns. This is done with the letter Z. At the end of the page, the names of the cashier and accountant are indicated. In addition, the number of receipt and account orders drawn up per day is indicated. If no cash transactions were performed in a day, the page is left blank. In this case, the balance available at the end of the day is carried over to the next without adjustments.

Electronic variant

The widespread introduction of computer technology did not pass by the cash book. The electronic version of the compilation of the magazine greatly facilitates the work of employees. To maintain the book uses a special program. It displays a log on a computer screen. The columns are filled in the same way as described above. Each day, the responsible employee enters the necessary information, and at the end of the shift prints a sheet. The paper version should have two parts: the report itself and the insert half. Cashier signs the page. If the employee has an electronic signature, then it is allowed to use it, as well as the usual one. Each such page is numbered. At the end of the year, a book of printed sheets is formed. On its last page the total number of inserts is indicated. It is certified by the signatures and seal of the enterprise. An e-book is allowed to be compiled once a quarter, and not annually. Reports and attached documentation are sent to the finance department.

Income and expense

Cash receipt is made out by cash receipt order. The receipt - its detachable part - must be filed with the bank statement. Disposal operations are executed, respectively, by one or more account orders. Upon delivery of cash to the bank, the employee is issued a receipt and an order. The first is filed to the cashier, and the second to the statement.

Log fixes

If a mistake was made in the book that does not have a significant effect on the reporting, it can be corrected. It is strictly forbidden to tear out sheets from the magazine. The use of a stroke, a marker, wiping with a blade, an eraser and other similar manipulations is also not allowed. If the slip does not entail a change in the balances of any period, then its correction is carried out as follows: the incorrect entry is crossed out neatly, the correct one is placed next to it. The adjustment must be certified by signatures. The cashier and accountant must sign it. If there are several corrections on the page, then each of them must be certified. If a serious mistake is made, the cashier draws up a statement addressed to the chief accountant. The head of the enterprise is going to a commission that will be responsible for corrections. Based on the mistake made, an accounting statement is drawn up. It describes the nature of the inaccuracy and the method for correcting it.

Verification of reporting discipline

The correctness of the cash register is entitled to be monitored by the banking organization serving the account of the enterprise. That the check will be carried out, the head is notified by notification. For the assessment, it will be necessary to provide the deposit sheets fully executed, the cashier's reports together with the attached documentation, and advance papers if the money was issued against the report. If the check will affect the current year, there is no need to stitch the journal (this is done at the end of the year). Upon completion of control measures, the book will be returned to the enterprise. In this case, the authorized body will issue an act on the verification of reporting discipline. If the document contains comments, they must be eliminated by the deadline set by the regulatory body. Also, the tax office can check the accuracy of filling out the cash book. For violations identified during control measures, sanctions may be applied. It should be noted that the inspector may impose a fine on the enterprise if errors were identified within two months from their admission.