Changes in tax legislation that came into force from the beginning of 2017 led to the fact that the administration of almost all mandatory payments to off-budget funds turned out to be assigned to the tax authorities. The only exception was contributions for compulsory insurance against industrial accidents, colloquially for injuries. They are still fully engaged in social insurance.

Changes in reporting

The tremendous change in revenue administrators naturally led to a change in reporting forms, thanks to desk audits which assess the discipline of paying contributions. Earlier reports were given:

- to the Pension Fund - for contributions to compulsory pension insurance and compulsory health insurance;

- to the Social Insurance Fund - for contributions for temporary disability insurance (for sick leave payments) and for injuries.

Now the tax authorities have developed their own form convenient for them regarding contributions to the OPS, to the FFOMS and to the FSS regarding contributions for temporary disability. Accordingly, social insurance from the old report of the 4-FSS excluded everything related to sick leave, and left only that related to injuries. Disability contribution reports are now one of the sections of the corresponding tax calculation. Thus, a new form of 4-FSS appeared.

4-FSS provision: dates and method of data transmission

Form 4-FSS is still provided by all organizations where, in accordance with the concluded agreement, employees work for wages. This applies equally to both state and private organizations, and individual entrepreneurs. The latter, if they do not have employees, pay these contributions at will and do not submit Form 4-FSS. A corresponding notice of the fund is not required.

The 4-FSS form can be filled out and submitted to the department of the fund, where the organization is listed on the registration, both in paper and in electronic form. That is, the transfer is carried out as a direct presentation, so through electronic communication channels. And there is an interesting nuance: the transfer can be made both through special operators, and directly through the official website of the FSS.

Reporting deadlines have not changed:

- in paper form - until the 20th day of the month following the reporting quarter;

- via electronic channels - until the 25th day of the month following the reporting quarter.

Sanctions for late reporting

If the completed 4-FSS form has not been received at the social insurance department on due dates for any reason, then the debtor is subject to the sanctions established by law: administrative fines are imposed on him. Both the organization and the official (most often the head) are fined. For the organization, the amount of the fine will be from 5 to 30 percent of the total accrual of contributions for the quarter, the data for which were not delivered on time (but not less than a thousand rubles), for the head from three hundred to five hundred rubles by decision of the justice of the peace.

How to fill out a report: innovations

A sample of 4-FSS filling in effect since October 2017 (the reporting period is nine months) is available on most accounting sites. Explanations for filling are on the official website of the FSS.

It contains a number of changes:

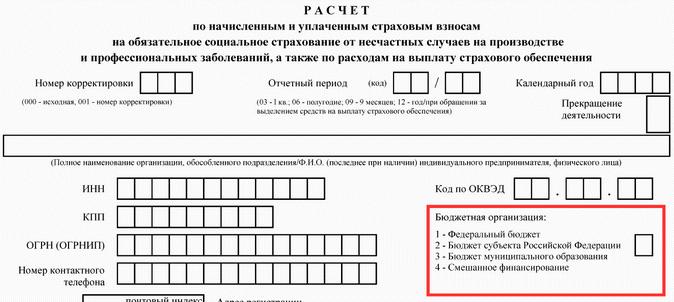

- on the cover page there is a field for data on the organization's affiliation to a certain budget level;

- the number of employees has been replaced by the average number of employees;

- in table 6 indicators instead of columns are distributed in rows;

- Table 2 does not need to separately fill out information on benefits issued to foreigners from the EAEU.

4-FSS: fill pattern

Under the new rules, all information regarding disability insurance contributions was excluded. Filling 4-FSS is carried out only in sections related to injuries. She became half shorter.

- On each page, an individual registration number must be indicated, which is in the notice of registration as the policyholder who assigned the fund.

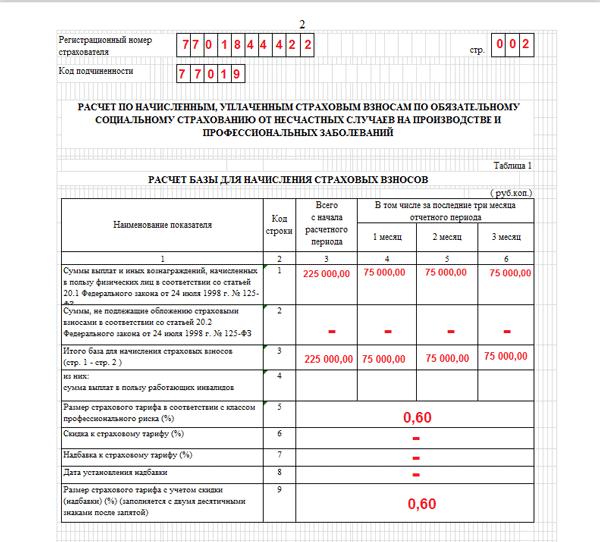

- Table 1 shows the estimated basis for contributions for insurance against injuries and occupational diseases. The value of the tariff is associated with the class of professional risk, which is assigned to the organization in accordance with the norms of the current legislation in accordance with OKVED, recorded in the charter documents of the enterprise. The class is usually indicated in the corresponding notice from the FSS issued upon registration of a legal entity as a payer. There can be several classes - depending on the number of activities. If the class is one, then 4-FSS is completed once. If there are units with different classes, then the calculation is filled as many times as there are classes.

- Table 1.1 represents only those legal entities that for a certain time transfer their employees to other organizations.

- Table 3 is completed if payments were made on sick leave issued due to work-related injuries or occupational diseases, or money was spent on injury prevention. The entire list of expenses can be found in Law 125-FZ. The costs of special assessment should be reflected in this section only if they were authorized by the fund. If the funds of the enterprise were not spent or expenses were incurred without the prior consent of the fund, then information about the costs is not reported. For permission of the fund for special assessment, guaranteeing subsequent compensation of costs incurred at the expense of social insurance, the application and the necessary package of documents are submitted to the fund until August 1. The application will be reviewed by the foundation and a decision will be made on whether to permit or prohibit a special assessment to pay injuries.

- Table 4 is filled in case of accidents at work.

- Table 5 shows the number of jobs that require special assessment.

Should I pass the null?

In the current work of organizations, there are situations when activities for some reason are not conducted or there are no employees. Accordingly, salary contributions are not charged or paid. But such cases do not exempt from reporting. Zero calculations are presented according to general rules. Filling out the 4-FSS form zero for a number of positions is absolutely no different from a regular report. Be sure to fill out the title and a number of tabular forms (1, 2, 5). The dates for passing the zero are the same.

What to do if errors are detected

In case of self-identification of errors made during the preparation of the 4-FSS report, it is necessary to correct them and notify the fund about new indicators. But the rule is only valid in cases where the calculated payments were underestimated. In cases of overstatement, there is no obligation to notify the fund. All relationships can be adjusted by providing the next calculation on an accrual basis.

In case of an underestimation, an adjustment is made to fill 4-FSS. A sample and explanations of the rules for making adjustments can also be found on almost all resources on the Web dedicated to accounting and on the official website of the FSS. The title necessarily indicates that this is an updated calculation and the adjustment number is indicated.

Important! When compiling the clarification, the exact form of the report that was in effect in the period when the calculation was submitted is applied. That is, if errors were discovered by 2016, then the form of that year is applied taking into account all sections related to sick leave. If mistakes are made precisely in the part of calculations on contributions for insurance claims for incapacity for work for 2016 and early periods, then the updated calculation should be submitted to the fund, and not to the tax one.

What is not the basis for calculating contributions

When drawing up the calculation, the responsible employee should remember that not all payments made to employees are taxed by injuries. The corresponding exceptions in the total expression must be reflected in table 6 of the calculation. Contributions to injuries are not charged on payments to foreigners temporarily residing in the territory of our state, and on the amount of disability benefits paid at the expense of the employer.

Important! At the conclusion of the contract, insurance contributions for disability payments are not charged, but injury insurance may well be one of the sections of the contract. In such cases, contributions are paid and information about them is included in the calculation.

Conclusion

Summarizing all of the above, it should be noted:

- Since 2017, the 4-FSS fill-out samples differ from the previous ones with the exception of the sections regarding sickness insurance contributions, which are now exclusively tax administered.

- The obligation to submit reports to the FSS remains, as well as the timing, forms and methods of reporting.